The Third Defensive Bucket: Managed Futures as an Alternative to Cash and Gold

The standard trend-filter recipe goes: hold leveraged equity (UPRO, TQQQ) when the underlying is above its 200-day SMA, otherwise sit in something safe. The "something safe" defaults to one of three things — cash, gold, or long bonds — and most retail strategies pick by gut.

The data picks differently. Over a 21-year window with the SMA200 filter on synthetic UPRO, gold beats cash by a hair, and long Treasuries (TLT, ZROZ) are the worst defensive option tested — worse than just holding cash. That's a result that catches most 60/40-trained investors off guard. The 2022 rate shock broke the equity/bond inverse correlation that traditional portfolio theory leans on; long bonds at 17-27 year duration are essentially a levered rate-shock bet now.

There's a fourth option worth considering: managed futures, specifically the iMGP DBi Managed Futures Strategy ETF (DBMF). DBMF tracks a trend-following CTA strategy across equities, rates, currencies, and commodities. It's designed to make money when something is trending, which means it's structurally different from buy-and-hold equity, gold, or bonds.

Most retail strategies don't include it. They probably should.

What the data says

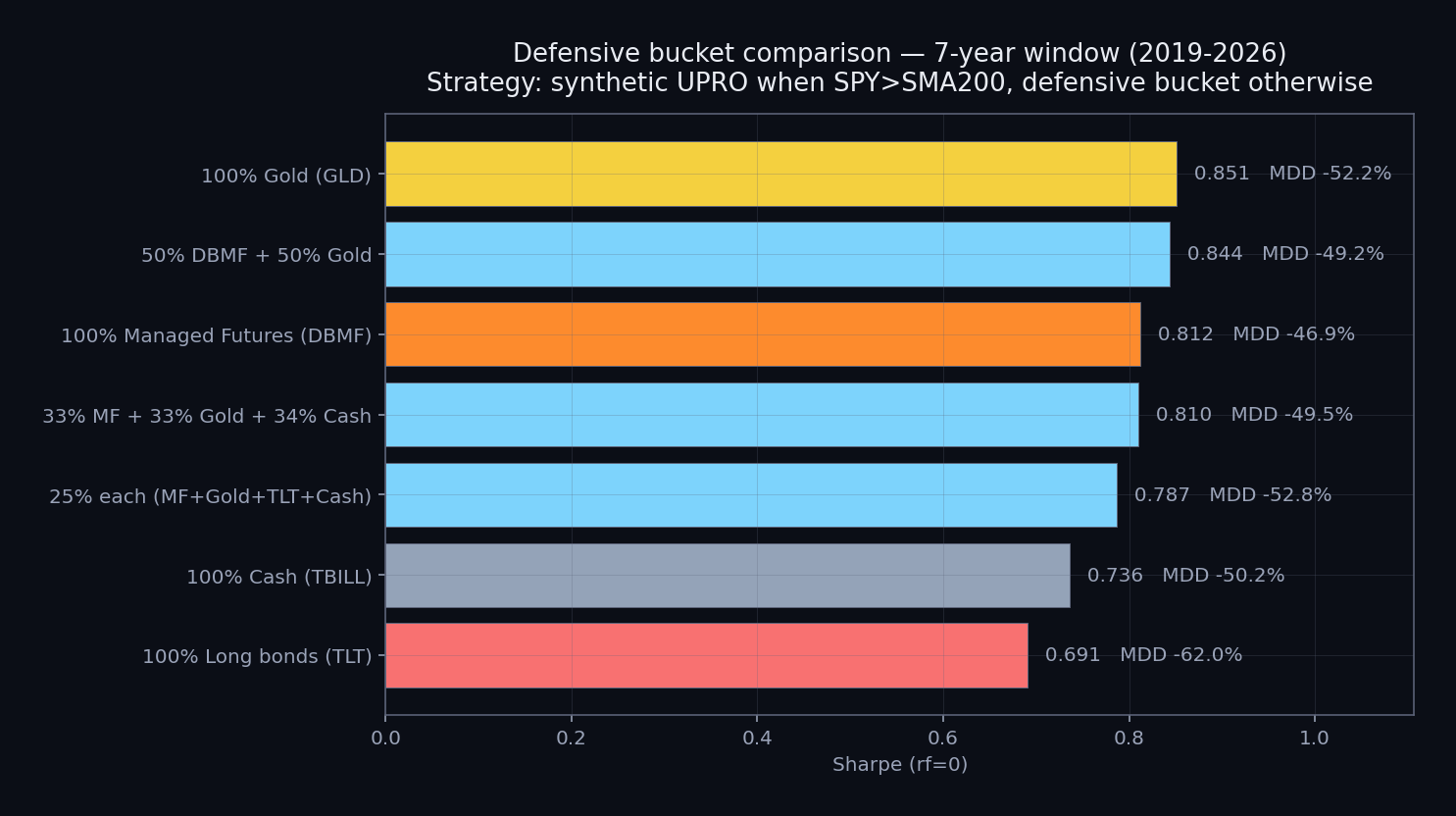

DBMF launched in May 2019, so we have 7 years of real-fund data to test (not synthetic). Same setup as before: 100% synthetic UPRO when SPY is above its 200-day SMA, defensive bucket otherwise. Borrow cost properly modeled on the leveraged sleeve.

The ranking (best Sharpe first):

| Defensive bucket | Sharpe | Max DD |

|---|---|---|

| 100% Gold (GLD) | 0.851 | -52.2% |

| 50% DBMF + 50% Gold | 0.844 | -49.2% |

| 100% Managed Futures (DBMF) | 0.812 | -46.9% |

| 33% MF + 33% Gold + 34% Cash | 0.810 | -49.5% |

| 25% each (MF + Gold + TLT + Cash) | 0.787 | -52.8% |

| 100% Cash (TBILL) | 0.736 | -50.2% |

| 100% Long bonds (TLT) | 0.691 | -62.0% |

Three real findings:

1. Pure gold wins on Sharpe. This is consistent with the longer-window defensive-bucket research covering 21 years. Gold's mild positive return plus its near-zero correlation with equity drawdowns makes it the cleanest single-asset defensive sleeve.

2. DBMF wins on max drawdown. -46.9% is the best of any defensive option tested. The mechanism: when the SMA filter exits the equity sleeve, DBMF tends to also be in trend-following mode and may be capturing the same regime change in different asset classes. In 2022 specifically, DBMF was long volatility, short equities, short bonds, and long energy — basically the inverse of a traditional 60/40 — and it returned roughly +20% in a year where most strategies fell apart.

3. The 50/50 DBMF + Gold combo is the sweet spot. Sharpe 0.844 (within rounding of pure gold's 0.851) AND max drawdown 49.2% (close to pure DBMF's 46.9%). You give up almost nothing on either axis vs the best single-asset, and you diversify across two very different defensive mechanisms.

The "25% each across MF + Gold + TLT + Cash" variant — which sounds intuitively balanced — is actually one of the worse options. Including TLT drags it down. The pattern from the earlier research holds: long bonds don't add defensive value in the post-2022 regime.

Why "trend following" works as defense

The mechanism is worth unpacking briefly because it's not intuitive.

A trend-following CTA strategy is long things that are going up and short things that are going down across many asset classes. When the equity market is in a calm uptrend, it's typically long equities — but so is the SMA filter, so they don't conflict. The interesting periods are when equities crash.

In a crash, three things tend to happen: equities fall (so the CTA is short), volatility spikes (so the CTA may go long VIX or equivalents), and macro flows shift (often into currencies or commodities). The CTA captures all three. Meanwhile your SMA200 filter has correctly exited the equity sleeve and is sitting in the defensive bucket — which, if that bucket is DBMF, is actively profiting from the same regime change.

Gold works through a different mechanism: flight to safety + dollar weakness + monetary fear. It's reactive to the same trigger but via different paths.

Combining gold and DBMF in the defensive bucket gives you exposure to both reactive paths. When the equity crash is inflation-driven (2022), MF wins via the rate trend. When it's a liquidity event (2008, 2020), gold wins via flight to safety. The combination hedges your hedge.

The regime caveat

The 7-year window includes 2020 (COVID), 2022 (rate shock), and the recovery. It's a regime that was uniquely favorable to managed futures — particularly 2022, where MF strategies were nearly the only asset class that made money. Whether DBMF continues to perform as well in a more typical regime is genuinely unknown.

A few honest concerns:

- 2022 was the headline year. Strip out 2022's outsized DBMF return and the Sharpe drops meaningfully. A future without another 2022-like rate shock would mean DBMF underperforms gold by more than the current numbers suggest.

- Trend-following CTAs have decade-long drought periods. The category went through 2009-2018 with minimal returns. If you're allocating based on the 2019-2026 window, you're sampling a particularly good chapter.

- The expense ratio matters. DBMF charges 0.85% per year, which eats into long-run defensive returns. Cash earns whatever T-bills pay (currently ~4-5%) with no fee.

The honest read: DBMF is a plausible third defensive sleeve based on a 7-year window that probably overrepresents its strengths. The longer-window research on gold + cash holds up across 21 years; the DBMF case has 7. Treat the DBMF edge as regime-dependent until a longer dataset confirms it.

Practical reads

If you're already running an SMA200 + leveraged equity strategy with a defensive bucket, this data suggests three actionable framings:

1. If you're currently in "100% cash" as your defensive bucket (the boring default), the data says adding gold or DBMF lifts Sharpe and improves drawdown. The pure-cash variant is the second-worst on the chart.

2. If you're currently in "100% TLT" or anything heavily weighted to long bonds, the data has been telling you to move for three years now. Long bonds at 17+ year duration produced the worst defensive results in both this 7-year window and the 21-year window in the deeper research. They're not defensive anymore; they're a rate-shock bet.

3. If you're currently in "100% gold," consider the 50/50 DBMF + Gold variant. You give up almost nothing on Sharpe, you gain a few percentage points on max drawdown, and you diversify across two different defensive mechanisms instead of one. If gold has a bad regime (1980s-style), DBMF would carry more of the load. If MF has a bad regime (2009-2018-style), gold would.

None of this is allocation advice. It's research output for the kind of person already running a trend-filter strategy and wondering how to think about the OFF position. The actual sizing depends on your tax situation, account type, time horizon, and risk tolerance — none of which a backtest can model.

What this article doesn't address

A few things worth flagging that this piece isn't arguing:

- DBMF in the equity sleeve, not just the defensive sleeve. Could a managed futures position be the equity sleeve substitute? Probably not for most people — DBMF doesn't have the same upside in bull runs as leveraged equity. But it's a more conservative variant of the leveraged-equity recipe.

- KMLM, CTA, and the other MF funds. This piece tests DBMF specifically because it's the most-traded retail managed-futures ETF. KMLM and others may behave differently. Cross-fund correlation studies are future research.

- Portfolio rebalancing cadence. All variants tested are daily rebalanced, which is unrealistic for tax-sensitive accounts. The rebalance frequency research shows yearly works nearly as well as daily on the broader portfolio; same likely true here.

Caveats worth naming

- 7-year window. Real DBMF only started in May 2019. We can't backtest further with this specific fund. Longer-window managed-futures index series (SG CTA, BTOP50) go back further and could be used as proxies; that's a future study.

- 2022 dominates the Sharpe story. Strip out 2022 and DBMF underperforms cash by a meaningful margin.

- Past performance is not predictive. Especially for trend-following strategies, which are explicitly regime-bets.

Source research

- Borrow-Cost Correction: Synthetic LETF Methodology + DBMF section — the underlying numbers powering this article's charts

- Defensive Bucket Comparison — the longer 21-year context for gold vs cash vs TLT (without DBMF, which lacks the data)

Reproducibility: every number from pip install sma200-bt + real-fund data via yfinance.

Related articles

- The Hidden Cost Every Leveraged-ETF Backtest Ignores — the borrow-cost methodology powering the synthetic UPRO sleeve used in these backtests

- Does the 200-day Moving Average Actually Beat Buy-and-Hold? — the foundational case for why the SMA200 filter is worth the trouble in the first place

- Why One Indicator Isn't Enough — the portfolio-construction angle that turns single-asset findings into actual strategies

Check current SMA200 status on the tickers discussed: DBMF, GLD, TLT, SPY, UPRO.

For the broker side of running a trend-filter strategy with multiple defensive sleeves, see the broker shortlist.